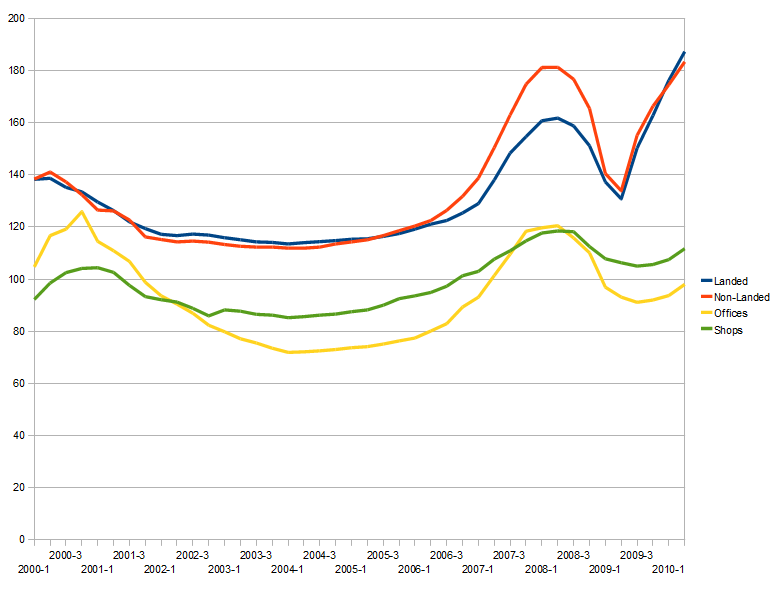

Let me start this article by diving right in and showing you the real estate prices in Singapore, quarter by quarter, as collected by the Urban Redevelopment Authority.

Pretty interesting right? Back in July 2009 I was actually thinking of buying a property there to take advantage of the prices finally going down. After a handful of visits I had to give up: things were becoming way too crazy for me. Prices would suddenly go up between the moment the ads were posted and the moment I would set a foot in the property for a visit. In one instance where I was trying to negotiate a condominium unit, the seller decided to raise his original asking price, rather than lower it to reach me halfway as you would expect in any negotiation. For the record, that property still hasn’t sold one year later, but the price has been raised again…

Pretty interesting right? Back in July 2009 I was actually thinking of buying a property there to take advantage of the prices finally going down. After a handful of visits I had to give up: things were becoming way too crazy for me. Prices would suddenly go up between the moment the ads were posted and the moment I would set a foot in the property for a visit. In one instance where I was trying to negotiate a condominium unit, the seller decided to raise his original asking price, rather than lower it to reach me halfway as you would expect in any negotiation. For the record, that property still hasn’t sold one year later, but the price has been raised again…

Obviously, from looking at the chart, my timing was wrong by just a few months as the market was in a sudden and unexpected rebound. We are now at record high prices for residential properties and as you can see, there’s no visible end in sight.

Some Local Surprises

For a foreigner like me, there are many surprising things about the local real-estate market. First thing is the incredibly low rental yields of properties: most private properties seem to yield only 3 to 4%, before taxes, agents and maintenance fees. In some older buildings, it is not rare to see yields of less than 2%! Once everything is paid, there’s probably little to no profit left. This makes no economical sense at all: these owners would be better off selling and investing that money somewhere else. If they insist on being in real estate, local real estate trusts (S-REIT) offer yields of 5 to 7% and provide the same opportunities of capital appreciation, without the hassle of managing a rental property and without paying high transaction fees or taxes.

The second thing is that the market is extremely speculative: condos which have been just completed have many units on sale, showing that a lot of owners are just looking to flip their unit for a quick profit. Many ads will list old units as having “en-bloc potential”, suggesting that a collective sale of the building for redevelopment could lead to high gains. It seems nobody believes that prices can do down… which of course is wrong if you get another look at the first graphic.

Thirdly, a lot of people have no qualms buying properties on a 99 year leasehold (these come from land sold by the government to developers). While they are quite cheaper than freehold (or the less common 999 years leasehold), they also come with the obvious long term depreciation (as the property will eventually be worthless when the lease runs up). But this depreciation is not linear, and the depreciation only becomes apparent after a few decades. This will be the subject of another article.

The fourth thing is that everybody wants new buildings: a condo from the 80s (or worse, 70s) will sell for a lot cheaper that ones delivered a few months ago. Granted, these buildings look less posh than the newer developments, but they are also more spacious. Obviously a premium is expected for a new unit but the premium here is in my opinion excessive.

Of course you also have the geography: land is scarce and Singapore is a haven of political stability in south-east Asia, so there’s a lot of pressure on prices and lots of cash-rich foreign buyers looking for a safe place to put their money.

Factors Affecting Prices

The first factor that affects prices is quite simply the government. Interestingly enough, the Singapore government monitors and tries to keep prices in check, and has recently on three occasions tightened up lending rules to limit the amount of speculation and leveraging (mostly by requiring bigger deposits), but this has not stopped people from gobbling up properties like there’s no tomorrow.

The second factor is, like in other countries, interest rates. They are incredibly low right now, as mortgages can be had for less than 2%. Most (if not all?) mortgages are offered as variable rate only, or with a fixed rate but only for a handful of years, so this makes the market very sensitive to any rates hike. Repaying your 1.8% mortgage with a property that yields 3.5% before taxes is easy and profitable, but when the rate goes to 3%, it becomes really hard. When the rate goes to 4%, you rush to sell your property… only to find out that buyers can’t borrow as much as they used to and hence have smaller budgets.

The graphic above shows non-landed private properties prices vs the 3 month SIBOR rate (interbank rate, often used as an index for variable rate mortgage), but as you can see a correlation isn’t as obvious as you might think at first.

The graphic above shows non-landed private properties prices vs the 3 month SIBOR rate (interbank rate, often used as an index for variable rate mortgage), but as you can see a correlation isn’t as obvious as you might think at first.

The third factor is the health of the stock market. Whereas in some countries a bad stock market will push investors into the “safe haven” of real estate, in Singapore things work the other way around and a good stock market makes investors hungrier for properties (which once again shows the speculative aspect of the local market). This is fairly obvious when you check the third chart below: non-landed properties vs the STI index.

Then of course there’s psychology. Local investors absolutely love real-estate and it is usually perceived as a safe and easy way of making money. Newspapers print ads for purchasing properties in Australia, Malaysia, U.K. or even Canada. Seminars are offered on how to “get rich quick” with real-estate investment. Going to show-flats on Sundays seems to be a classic family outing, of course the checkbook should not be forgotten for that condo impulse-buy!

Then of course there’s psychology. Local investors absolutely love real-estate and it is usually perceived as a safe and easy way of making money. Newspapers print ads for purchasing properties in Australia, Malaysia, U.K. or even Canada. Seminars are offered on how to “get rich quick” with real-estate investment. Going to show-flats on Sundays seems to be a classic family outing, of course the checkbook should not be forgotten for that condo impulse-buy!

Now what?

Obviously there’s no way to guess when new government rules will be introduced, but it’s doubtful that any increase of more than 10 to 15% year-on-year will be left unchecked, so we can at least consider that any further price increase will be somewhat moderated. Conversely, it wouldn’t be a surprise if rules were relaxed if prices started to fall. People aren’t happy if they can’t afford a house but they also don’t like to see their asset value fall down.

On the interest rates front, it seems “up” is the only way to go, but the question is “how high?”. Interest rates in US and Europe are likely to stay low for a long while, and it’s unclear to me how the rates in Singapore are going to move: you’d think that with the high GDP growth they would increase, but this has actually been the opposite. Also you’d need a good 1 or 2 points increase to really make a difference on real-estate investors who are leveraged to their eyeballs.

As to the stock market, your guess is as good as anyone else. Emerging markets are going full speed ahead and the Asians stock market might be in for a long bull run. Or maybe some bad news from Europe (sovereign bond crisis?) or the US will bring back the bears. It seems however that fears of a double dip have receded lately.

So to wrap this up: I do not believe the time is right to enter the Singapore residential real-estate market, unless finding a hidden gem offering a unusually high rental yield. The office and commercial markets look less exuberant than the residential (as they are mostly operated by professionals), so maybe there’s more potential there. I however do not expect prices to fall to the floor because there’s no visible economic change (rates or stocks) to pop the bubble.

How about for self stay. If we are paying 3000 rent and plan to stay for 5 years then what should be the strategy.

That really depends on the yield your landlord is getting from the rental. For example, buying a $1M house means you own a $1M asset that does nothing but saves you from paying rent. So it’s a form of investment (except it provides a saving rather than an income), which you have to compare to other forms of investments.

You should do the math and compare both options carefully, without forgetting the extra cost that comes with owning (property tax, maintenance fees, renovations, interests if you take a loan).

Another point to remember is that Singapore’s market is now really high – which means the chance of prices going down has increased. Buying is also a gamble on the market evolution.

Thanks for the reply. However the problem most savers are facing is where to safely park your funds for a good return. Stock markets are overrated and banks pay no interest so one feels that if you have enough for a deposit better to own than rent.

You are right – it’s not the best of times for savings, but there are still some opportunities around. For example Australian dollar term deposits can pay above 5%, Singapore REITs offer 5 to 8% yields, or alternatively some corporate bonds can pay above 5%. All of them carry some risks but I would say so does buying real estate at such high levels.

Very inspiring post, I can use this in my research with singapore property blog dedicated to helping you understand the real estate market and make better buying, selling, renting and investing decisions – minus all the hype and misinformation.